Editor’s note: This is a recurring post, regularly updated with new information.

At The Points Guy, we devote a significant amount of time to discussing how credit scores work and how to improve your credit score. Scores in the mid-700s and above will typically be enough to get you approved for most travel rewards cards. However, having a lower score doesn’t necessarily mean that you can’t get those cards.

In this guide, we’ll analyze data points to uncover the unpublished (and perhaps unofficial) credit score requirements for the ever-popular Chase Sapphire Preferred Card, which is currently offering an enhanced sign-up bonus of 80,000 bonus points after you spend $4,000 on purchases in the first three months from account opening.

Just note that although your credit score is a good indicator of your approval odds, it’s not an absolute science. Chase may still deny you even if you meet the “required” credit score — and may still approve you even if you’re below it.

Chase Sapphire Preferred overview

The Chase Sapphire Preferred Card is a longtime favorite among advanced points and miles collectors. If you’re considering adding it to your wallet, now is a great time to do so.

The Sapphire Preferred earns valuable Chase Ultimate Rewards points that can be transferred to the program’s hotel and airline partners. It also comes with perks like an annual $50 hotel credit for reservations made through Chase Travel and a 10% points bonus on your cardmember anniversary.

Check out the full Chase Sapphire Preferred credit card review for more information.

Application link: Chase Sapphire Preferred Card

Credit score needed for the Chase Sapphire Preferred

The Chase Sapphire Preferred is considered a great beginner card, but you may not get approved if you don’t have much credit history or only have one credit card to your name. I’d recommend applying for one of the best first credit cards or best credit cards for college students if you are brand-new to credit cards.

However, it’s certainly possible to be approved for the Chase Sapphire Preferred as a beginner. According to Credit Karma, Chase Sapphire Preferred’s average required credit score is 736. The typical low score is 646. So, while the average score for approvals is “good” to “very good,” perfect credit history isn’t necessary.

Many other factors go into qualification beyond your credit score, such as your income and the average age of your credit accounts. Another significant factor that’s often forgotten is your relationship with the bank. If you’ve been a longtime Chase customer and have large balances in your bank accounts with them, reports suggest that you may have better approval odds (especially if you apply in a branch).

Finally, even if you’re eyeing the Chase Sapphire Reserve, you may want to apply for the Chase Sapphire Preferred first. After all, getting approved for the Sapphire Preferred is generally easier than the Sapphire Reserve. Also, applying for the Chase Sapphire Preferred now will allow you to earn that sign-up bonus of 80,000 points. Then, if you want to utilize the perks on the Sapphire Reserve at a later date, you can request a product change.

Related: Can you downgrade and then upgrade the same card?

How many card accounts can I have open?

As with most Chase cards, the Chase Sapphire Preferred is subject to Chase’s 5/24 rule. The 5/24 rule means that Chase will automatically reject your application if you’ve opened five or more personal credit cards (with any issuer) in the last 24 months.

The 5/24 rule is hard-coded into Chase’s system, so agents generally can’t manually override it. As such, if you’re over 5/24, your only option for getting the Chase Sapphire Preferred is to wait until you’re under 5/24 again.

Related: How to calculate your 5/24 standing

How to check your credit score

Under no circumstances should you pay to check your credit score. Many credit cards come with a free FICO score calculator. Also, there are many other ways to check your credit score for absolutely free.

Many free sites can help you keep better track of your score and its factors. You can even use these services to dispute any information on your score that isn’t accurate or appears to be fraudulent. You could also consider paying for a credit monitoring service like myFICO.

Factors that affect your credit score

Before you start applying for any credit cards, it’s essential to understand the factors that make up your credit score. After all, the mere act of applying for a new line of credit will change your score.

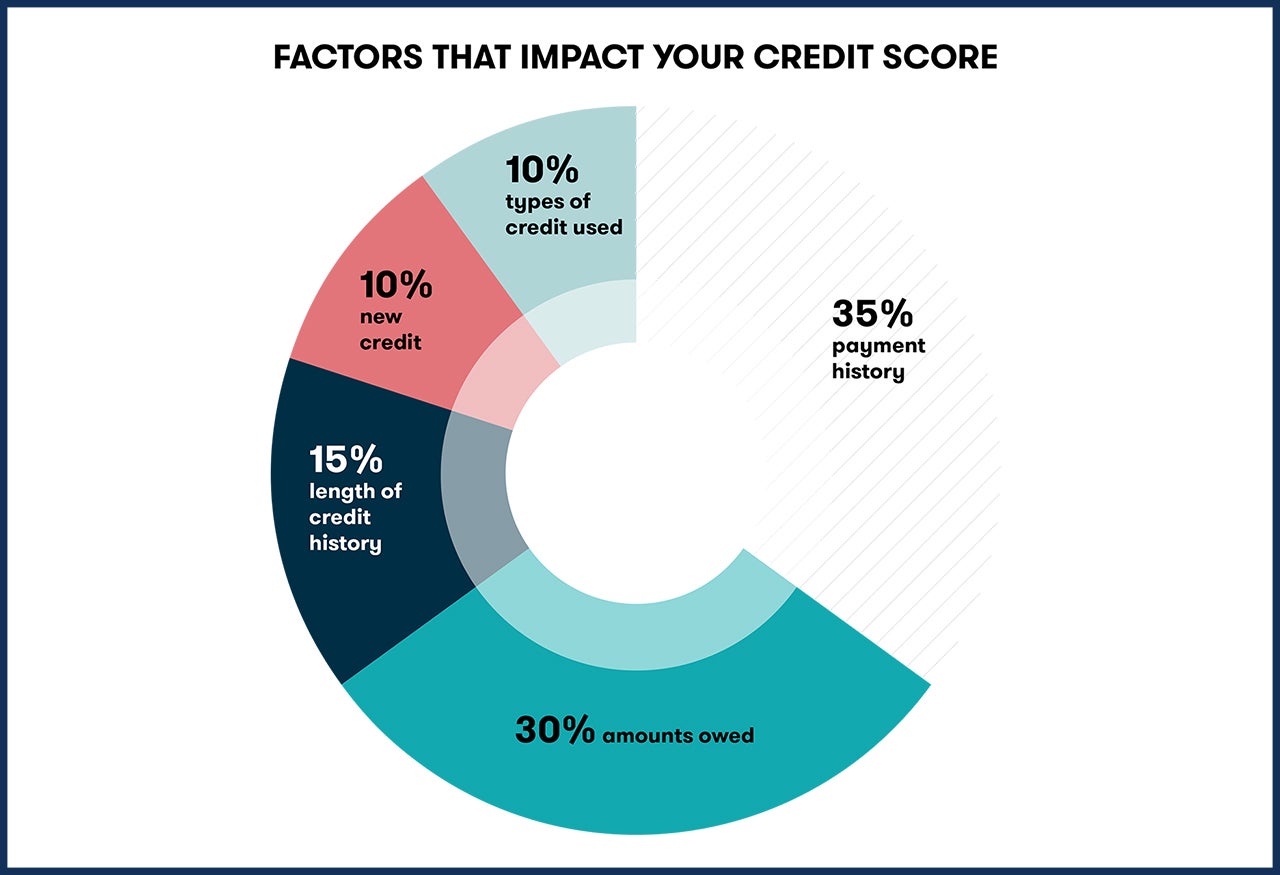

While the exact formula for calculating your credit score isn’t public, FICO is transparent about the factors they assess and the weightings they use:

- Payment history: 35% of a FICO score represents your payment history. So, if you get behind in making loan payments, this part of your credit score will suffer. Also, the more extended and more recent the delinquency, the more significant the negative effect.

- Amounts owed (credit utilization): 30% of your FICO score consists of the relative size of your current debt. In particular, your debt-to-credit ratio is the total of your debts divided by the total amount of credit available across all your accounts. Many people claim that it’s best to have a debt-to-credit ratio below 20%, but it’s not a magic number.

- Length of credit history: 15% of your score represents the average length of all accounts on your credit history. The average length of your accounts can be a significant factor if you have a limited credit history. It can also be a factor for people who open and close accounts quickly.

- New credit: Your most recent accounts determine 10% of your credit score. So, this part of your credit score will suffer if you’ve recently opened too many accounts. After all, obtaining a lot of new credit is one sign of financial distress.

- Credit mix: 10% of your score is related to how many different credit accounts you have, such as mortgages, car loans, credit loans and store credit cards. While having a mix of loan types is better than having just one type, no one recommends taking out unnecessary loans solely to boost your credit score.

With regard to the Chase Sapphire Preferred, one crucial factor to consider is your average age of accounts. While a lengthier credit history will boost your score, many issuers focus on the one-year cutoff. That means that having an average age of accounts of more than a year can go a long way toward increasing your odds of approval. However, you might have trouble getting approved with 11 months of credit history — even if your numerical credit score is excellent.

Finally, if you have any delinquencies or bankruptcies on your credit report, Chase might hesitate to approve you for a new line of credit. It’s important to remember that your credit profile is more than just a number. Indeed, your credit profile is a collection of information given to the issuer to analyze your creditworthiness.

As a result, there’s no hard-and-fast rule with a specific credit score that will automatically get you approved (or denied) for the Sapphire Preferred.

Related: 7 things to understand about credit before applying for a new card

What to do if you get rejected

If Chase rejects you for a credit card, don’t give up. Credit card issuers have rejected me for 10 to 15 different credit cards over the years. While it hurts, you need to learn to fight for yourself. If you receive a rejection letter, you should first examine the reasons for your rejection. By law, card issuers must send you a written or electronic communication explaining what factors prevented you from being approved.

Once you’ve figured out why Chase rejected you, you can call the reconsideration line. Tell the person on the phone that you recently applied for a Chase credit card, were surprised to see Chase rejected your application and would like to speak to someone about getting that decision reconsidered. From there, it’s up to you to build a case and convince the agent why Chase should approve you for the card.

For example, if Chase rejected you for having a short credit history, you can point to your stellar record of on-time payments. Or, if Chase rejected you for missed payments, you could explain that those were a long time ago and your recent history has been perfect.

Related: Your guide to calling a credit card reconsideration line

Chase is also known to limit a customer’s total credit line across all cards. You may have success overcoming a rejection by offering to shift unused credit from an existing card to the new one.

There’s no guarantee that your call will work, but about one-third of my rejections were reversed on reconsideration. So, it’s worth spending 15 minutes on the phone if it might help you get the card you want.

Bottom line

The Chase Sapphire Preferred Card is a great option for those just getting started in the world of points and miles, especially with the current 80,000-point sign-up bonus. Hopefully, you won’t have trouble getting approved. But keep in mind that Chase will likely automatically reject you if any of the following apply to you:

- Already have a Sapphire card (including the Chase Sapphire Reserve and the no-annual-fee Sapphire card, which is no longer accepting new applicants).

- Received a sign-up bonus from any Sapphire card in the last 48 months.

- Opened five or more cards across all issuers in the last 24 months.

Although the average approved credit score is relatively high, you shouldn’t let that scare you away. After all, Chase will consider many other factors. Your best bet for keeping your score on a successful track is making on-time payments, keeping your closing balances low and being smart about the accounts you open and close. Establishing a banking relationship with Chase can also help your case. As the saying goes, though, your mileage may vary.

Official application link: Chase Sapphire Preferred Card

Additional reporting by Ryan Wilcox and Benét J. Wilson.